|

Treasuries |

|

|

|

|

Treasuries |

|

|

Treasuries

|

Treasuries |

|

|

|

|

Treasuries |

|

|

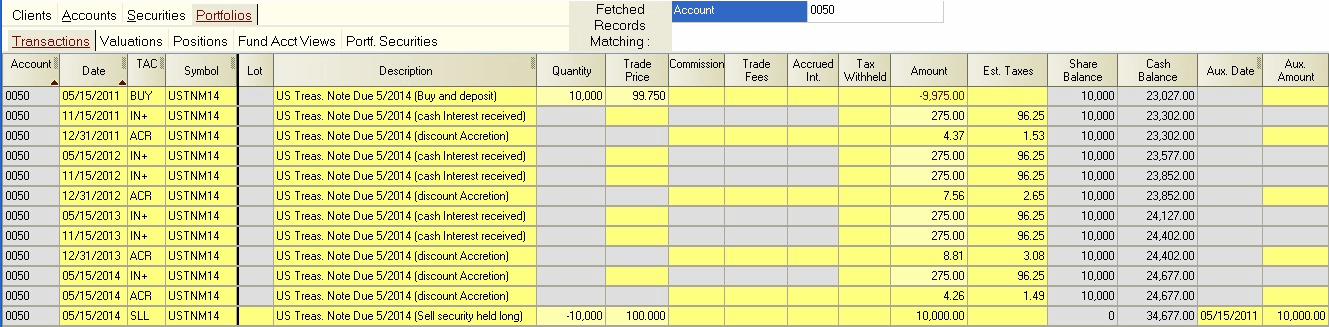

The treatment of investments in United States Treasury securities varies depending upon the type of security. Treasury notes and Treasury bonds are treated like bonds. For example, assume you purchased a $10,000, 5.5% three year note at one of the regular Treasury auctions or through the Treasury Direct program. Assume that it is purchased at a slight discount price of 99.75 and you hold the note until maturity. The transactions would appear as follows:

The ACR transactions are used to "accrete" the original issue discount so that there is no capital gain once the bond matures. If the bond had been purchased at a premium, an AMT amortization transaction would be used in lieu of the accretion transactions. U.S. tax law requires taxes be paid on accreted discounts, and conversely, permits a reduction in taxes due to amortized premiums. See Bond Discounts & Premiums for more details on these types of transactions.

Accrued Interest - If a Treasury note or bond is purchased or sold in the secondary market, the purchase and/or sale should include accrued interest paid on the purchase, or received from the sale of the bond. Consider a $100,000, thirty year, Nov. 2019 Treasury bond which is purchased at a premium and then later sold on the market prior to maturity. Both the purchase and sale transactions contain accrued interest as shown in this example:

Note that this example also shows amortization transactions.

Accreted Interest - Treasury Bills are Treasury debt with 52 weeks or less of maturity at issue. These are normally sold at a discount and redeemed at maturity for face value. The ACR (accretion) transaction is used to accrete the discount in a fashion similar to a zero coupon bond. This is illustrated in the following example involving a 52 week bill: